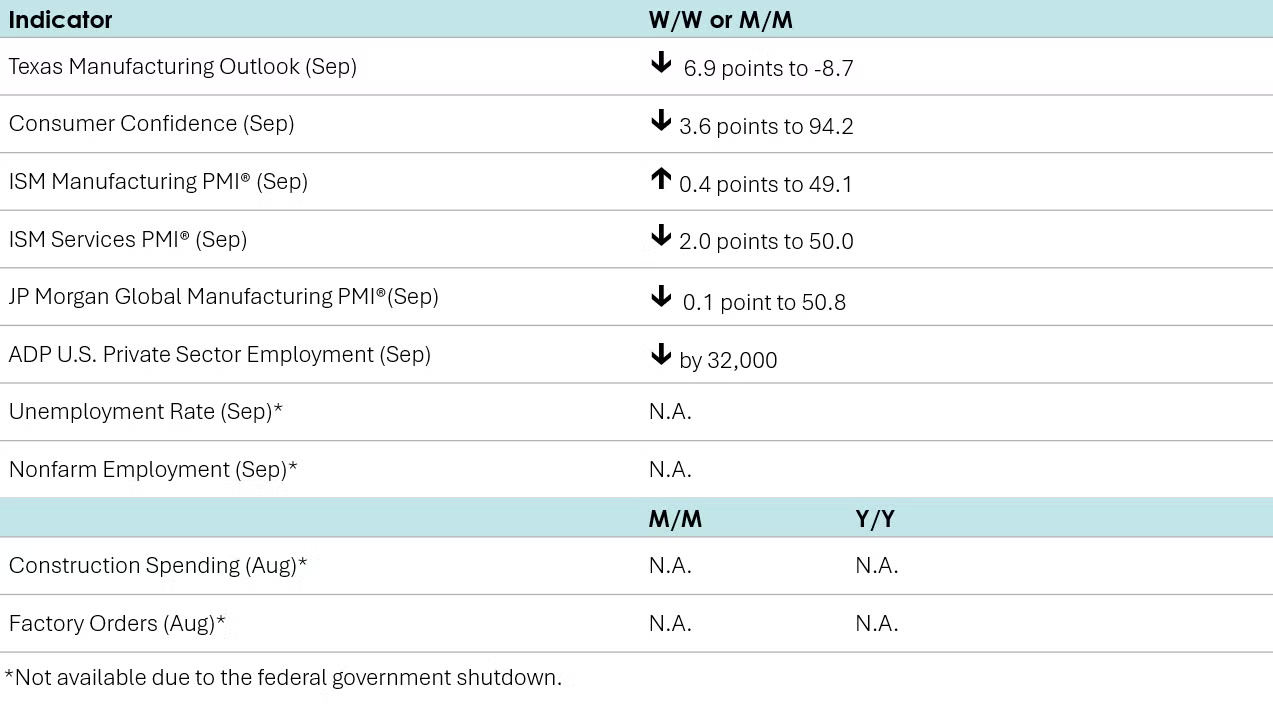

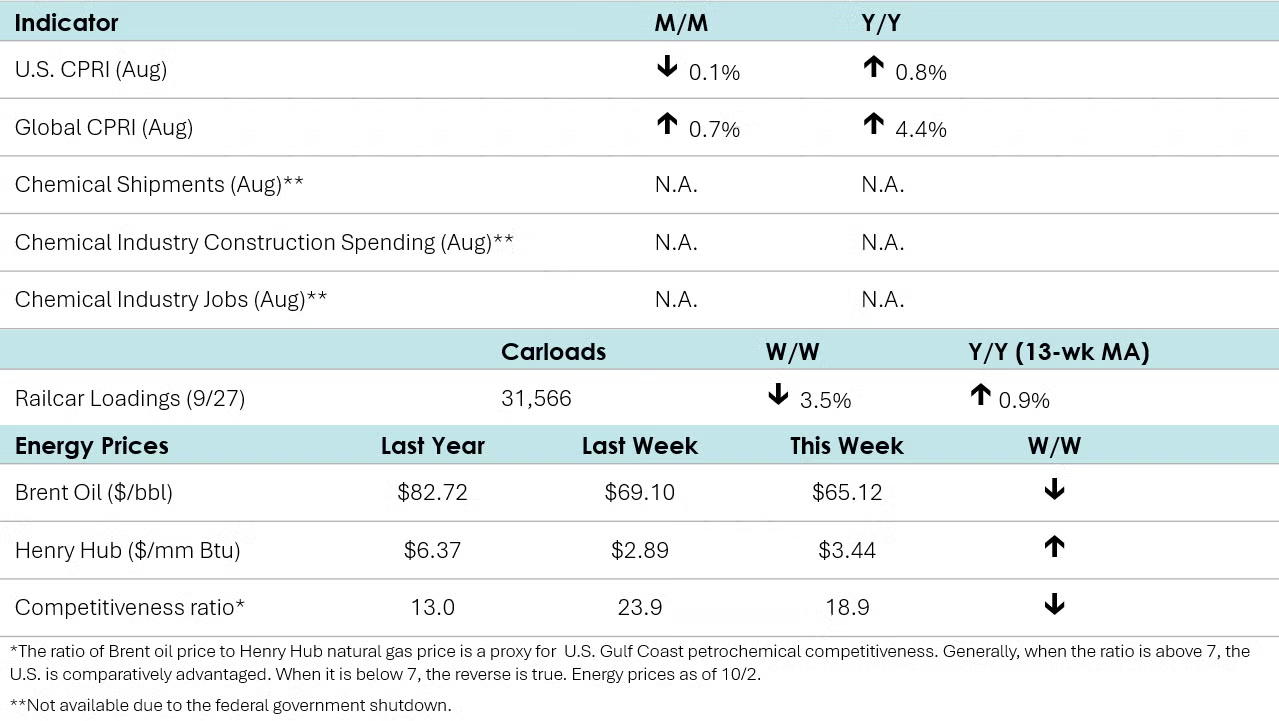

Note: Construction Spending, Factory Orders, Nonfarm Employment, and the Unemployment Rate were scheduled for release this week but are unavailable due to the federal government shutdown. Where available, we will include alternative private-sector data in order to continue monitoring the U.S. economy.

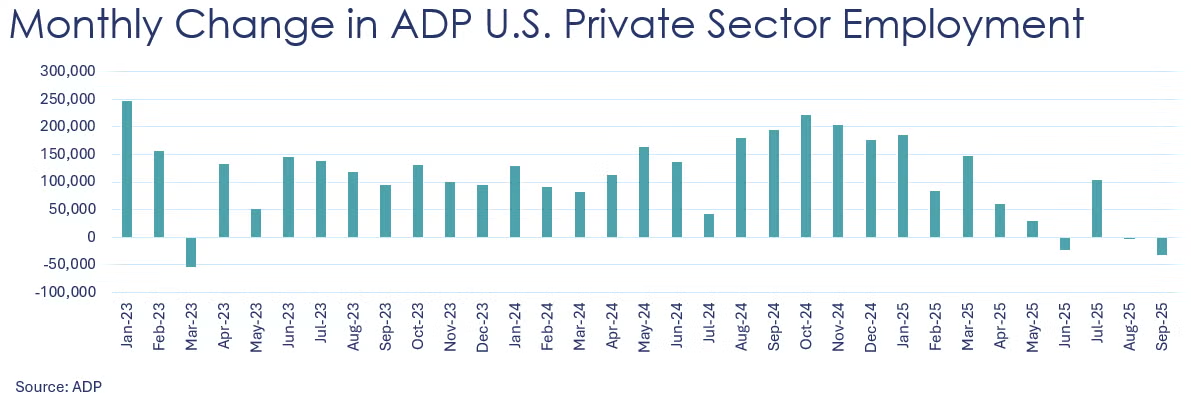

A proxy for the BLS nonfarm payrolls data, ADP reported that U.S. private sector employment fell for a second month, down by 32,000. Among size classes, only very large employers (with 500+ employees) added to payrolls. Job gains in natural resources & mining; information; and education & health services were offset by declines in other segments, including manufacturing which was down by 2,000. The ADP National Employment Report is an independent and high-frequency view of the private-sector labor market based on the aggregated and anonymized payroll data of more than 26 million U.S. employees.

Separately, The Challenger Report® showed that announced job cuts by U.S.-based employers in September were 37% lower than in August and 26% below year ago levels. On a year-to-date (YTD) basis, job cuts totaled over 946,000, the highest YTD level since 2020. The report notes that during the first nine months of the year, the government sector accounts for around a third of planned job cuts while technology, retailers, and media companies have also announced significant cuts so far this year. Employers’ hiring plans through September were down 58% compared to the first nine months of 2024.

Job openings remained essentially unchanged at 7.2 million in August, the lowest level since last September and, except for that month, the lowest since the pandemic. Total separations, including quits and layoffs, were also flat from July.

Consumer confidence declined in September, with the index down 3.6 points to 94.2, the lowest since April. Expectations worsened across two components: business conditions and employment prospects, while improving slightly for future income. Since February, expectations have been at levels which typically indicate a recession is ahead, the Conference Board reported. Purchasing plans for cars declined while plans for buying homes rose to a four-month high. Plans for purchasing big-ticket items remained somewhat unchanged overall, although there was an increase in plans for buying electronic goods, especially smartphones. Plans for purchasing appliances appeared mixed.

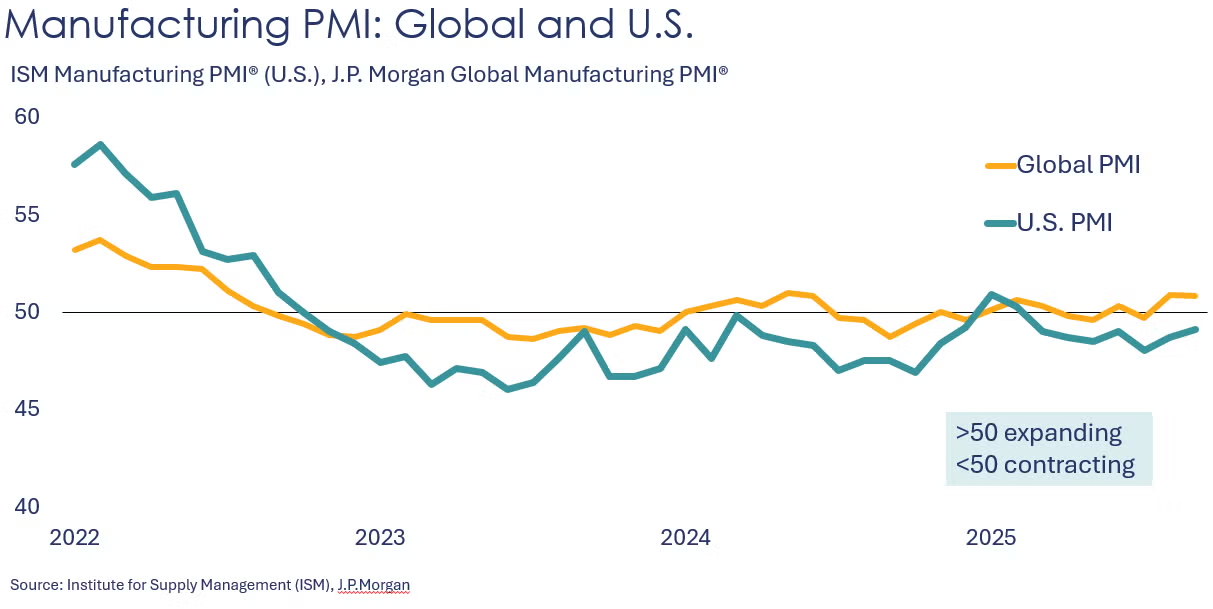

The ISM Manufacturing PMI® rose 0.4 points to 49.1 in September, the seventh consecutive month below 50 which indicates manufacturing activity contracted, though at a slower pace than in August. Production expanded, though new orders eased (following an expansion in August). Export orders, imports, order backlogs, employment and inventories continued to contract. Supplier deliveries were a little slower. Customers’ inventories continued to be assessed as “too low.” Five manufacturing industries reported growth while 11 reported contractions.

Looking abroad, the JP Morgan Global Manufacturing PMI ticked slightly lower in September, down 0.1 points to 50.8. The above 50 reading suggests that global manufacturing continued to expand in September. There was expansion across consumer, intermediate, and investment goods categories for a second consecutive month. India saw the fastest growth while manufacturing in China accelerated. The Eurozone fell back into contraction (following a brief expansion in August).

The Dallas Fed’s Texas Manufacturing Outlook Survey showed that manufacturing activity continued to grow in September, although at a slower pace than the previous month, as the production index fell 10.1 points to 5.2. The general business activity index fell seven points to -8.7. New orders contracted (following expansion in August). Unfilled orders continued to contract, as did finished goods inventories. Outlook uncertainty was slightly lower. Looking ahead six months, expectations for Texas manufacturers remained positive but tapered off from August.

The ISM Services PMI® dipped September, losing two points and reaching the breakeven level of 50, indicating neither expansion nor contraction in the services sector. The decline was led by imports, inventories, and business activity/production, which switched from expansion in August to contraction. New orders expanded at a lower rate, while employment and backlog of orders continue to contract but at slower pace. Supplier deliveries slowed further, while prices accelerated slightly. Inventory sentiment remained “too high”.

Within the details of the ISM Manufacturing PMI® report, the chemical industry was reported to be in contraction. New orders, production, employment, inventories, order backlogs, export orders, and imports. The chemical industry reported slower supplier deliveries. While the chemical industry assessed its customers’ inventories as “too low”, downstream plastic & rubber products said their customers’ inventories were “too high.” One chemical industry respondent noted, “The tariffs are still causing issues with imported goods into the U.S. In addition to the cost concerns, product is being held up at borders due to documentation issues. The inflation issues continue; low volumes are a constant concern. The European region is not improving as we had expected, causing further concern for long-term business viability.”

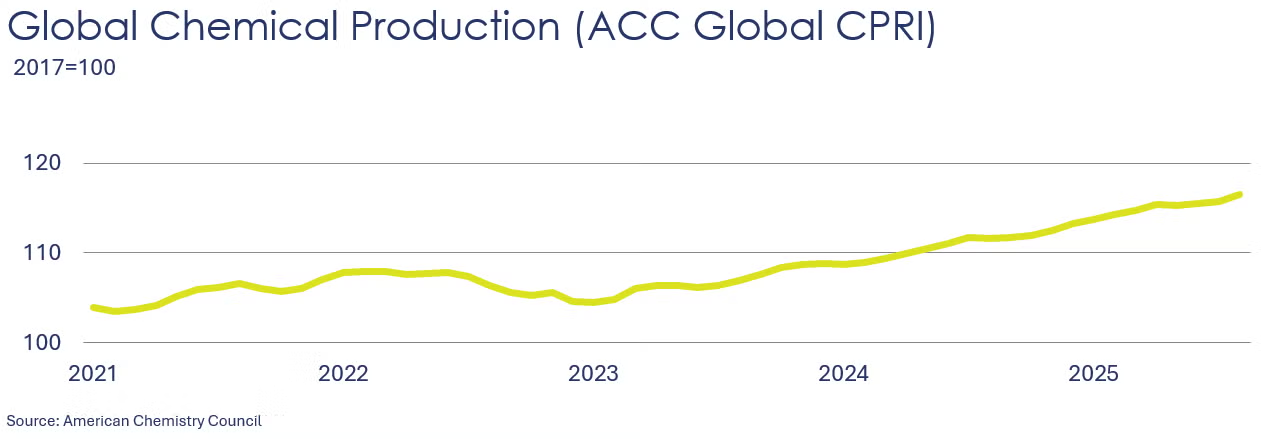

Following a 0.2% gain in July, ACC’s Global Chemical Production Regional Index (Global CPRI) accelerated in August with a 0.7% increase. Production in Asia and South America gained while the rest of the world declined. China’s production accelerated after three months of lackluster growth, possibly reflecting renewed strength in EV exports. Despite improvement in industrial demand, U.S. chemical production continued to fall as trade-related uncertainty continued to weigh on customer demand. Germany’s output improved this month, but a slowing PMI suggests uncertain momentum. Brazil's production gained 2.3% despite economic uncertainties. On a segment basis, all segments demonstrated strength, with agricultural chemicals leading the way. Global chemicals production growth was up 4.4% year over year.

Following gains in July, the U.S. CPRI declined by 0.1% in August, marking the seventh consecutive decline in eight months. The U.S. CPRI measures chemical production trends on a three-month moving average (3MMA) to smooth month-to-month volatility. Chemical production was down in all regions except the Gulf Coast. The U.S. CPRI was 0.8% higher than a year ago.

Energy Wrap-Up

• Oil prices were higher on growing concerns about oversupply (including plans by OPEC+ to boost production).

• U.S. natural gas prices were higher as the front month moved to November.

• The combined oil & gas rig count rose for a fourth week, up by five to 541.

For More Information

ACC members can access additional data, economic analyses, presentations, outlooks, and weekly economic updates through ACCexchange: https://accexchange.sharepoint.com/Economics/SitePages/Home.aspx

In addition to this weekly report, ACC offers numerous other economic data that cover worldwide production, trade, shipments, inventories, price indices, energy, employment, investment, R&D, EH&S, financial performance measures, macroeconomic data, plus much more. To order, visit http://store.americanchemistry.com/.

Every effort has been made in the preparation of this weekly report to provide the best available information and analysis. However, neither the American Chemistry Council, nor any of its employees, agents or other assigns makes any warranty, expressed or implied, or assumes any liability or responsibility for any use, or the results of such use, of any information or data disclosed in this material.

Contact us at ACC_EconomicsDepartment@americanchemistry.com.