Looking ahead the U.S. economy will drive up demand across many key chemistry end-use industries, which should tee up a healthy increase in chemical output. This promising outlook is dampened by the rising regulatory impact on the chemical industry, which threatens to undermine America’s competitive advantages in energy and the potential growth generated by the rebound in U.S. manufacturing.

Economy Maintains Momentum

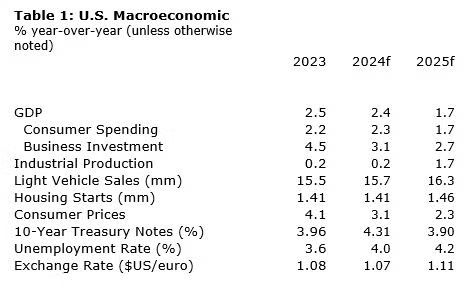

Moving into mid-year, the U.S. economy is on solid footing. While Q1 GDP came in weaker than expected, it was softer net exports and inventory investment that offset stronger activity in the domestic economy. Inflation unexpectedly accelerated in Q1 before resuming its downward trend and expectations for interest rate cuts have likely been pushed back toward the latter part of the year. We expect U.S. GDP to rise 2.4% in 2024, before slowing to a 1.7% gain in 2025.

Consumer spending has remained relatively resilient thus far in 2024 on rising real wages and confidence in the labor market. The engine of consumer spending is expected to downshift, however, as households contend with higher borrowing costs, slowing wage gains, and the exhaustion of accumulated pandemic savings. The composition of consumer spending also remains tilted toward services rather than goods, with important implications for goods-producing sectors, like chemicals. Following a 2.2% gain in 2023, we expect growth in consumer spending in 2024 of 2.3%, before slowing to a 1.7% pace in 2025.

Business investment, motivated, in part, by recent legislation (e.g., Inflation Reduction Act, CHIPS Act), rose 4.5% in 2023. With higher borrowing costs and tighter credit conditions, growth is business investment is expected to slow to 3.1% in 2024 and 2.7% in 2025.

Job growth has slowed as one of the tightest labor markets in recent history is starting to loosen. Wage growth, which drives income growth for most Americans (and subsequently their ability to spend) has slowed and is expected to continue to ease as the labor market rebalances.

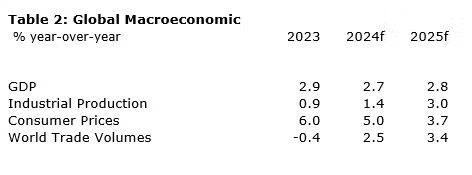

The global economy is expected to grow by 2.7% this year. The expansion will be supported by persistence in the US economy. Global GDP is forecast to increase at a steady 2.8%-2.9% pace through the end of our forecast period (2032).

Industrial activity has been weak worldwide. This year we should see a modest recovery. Global industrial production growth is forecast to increase by 1.4% this year (2024) before accelerating to 3.0% growth in 2025.

Following a small contraction in 2023, world trade volumes will recover modestly, growing at a 2.5% pace this year (2024) before accelerating slightly to a 3.4% pace in 2025.

Moderate Gains in Chemical Demand

The majority of basic and specialty chemicals are consumed by the industrial sector and the outlook for industrial production, while improved compared to 2023, remains comparatively weak. Overall industrial production rose just 0.2% in 2023 and a similar modest gain is expected in 2024 before rising by 1.7% in 2025. Led by a recovery in consumer goods and investment gains, industrial production is expected to expand more during the second half of the year.

Following 16 months of consecutive contraction, U.S. manufacturing expanded in March according to the ISM Manufacturing PMI®, but fell back into contraction territory in April and May. Performance in the industrial sector has been uneven. We anticipate a turnaround this year with 12 of the 18 key chemistry end-use industries we track expanding in 2024. Industries tied to automotive, aerospace, and electrical/electronics fare the best, while industries linked to housing and industries in structural decline (textiles, apparel, etc.) are expected to continue to struggle for the rest of the year.

The average automobile built in North America contains more than $4,400 of chemistry products (including 426 lbs of plastics and composites) making it an important end-use industry for chemical producers. Following four years of below-average sales, there is pent-up demand for vehicles. With higher borrowing costs and uncertain economic conditions, growth in vehicle sales is expected to edge slightly higher to 15.7 million in 2024 and 16.3 million in 2025. Electric vehicles (which are expected to account for 10% of sales by the end of 2024 according to Cox Automotive) contains 85% more chemistry (by value) than internal combustion engine (ICE) vehicles.

With 33,000 pounds of chemistry products in the average single-family home built in the U.S., another important end-use market for chemistry is housing. New homebuilding was especially hard hit when the Fed began to raise interest rates in March 2022. However, with the vast majority of homeowners “locked” into low mortgage rates, low inventories (and high prices) of existing homes have driven some potential homebuyers to the market for newly built homes, providing some support for housing starts. Housing starts are expected to be essentially flat in 2024 at 1.41 million units before rising to 1.46 in 2025 as interest rates begin to ease.

Chemical Production Grows in 2024

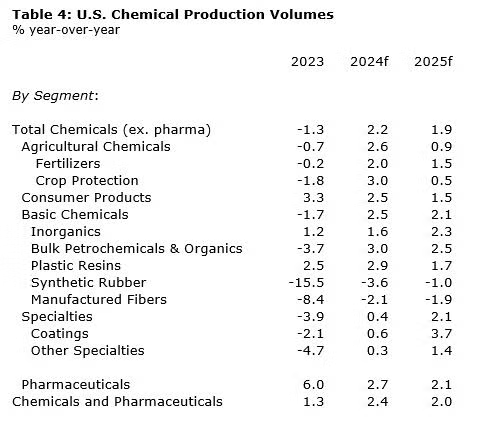

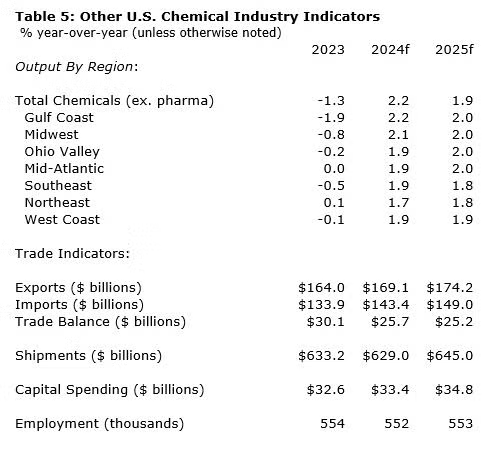

The past year was a tough one for chemical producers as an unprecedented destocking cycle curbed production, which was down 1.3% in 2023. With inventories in a more balanced position and nascent signs of firming demand in several end-use markets, we expect chemical output volumes to grow by 2.2% in 2024 with gains across all segments. Output is expected to grow 1.9% in 2025. Within the U.S., the largest gains are expected in the Gulf Coast and Midwest regions.

This is consistent with the findings of ACC’s Economic Sentiment Index that found chemical firms felt that overall business activity and major customer demand improved in Q1 and are expected to continue to improve over the next six months. Because of the chemical industry’s early position in the supply chain, we would expect to see a turnaround in chemicals before improvement in the broader economy.

We anticipate output of basic chemicals in the U.S. to rise 2.5% in 2024 with gains in petrochemicals and organic intermediates, inorganic chemicals, and plastic resins. Plastic resins output will continue to grow, up 2.9% in 2024, in part due to stronger exports. Specialty chemical output is also expected to rise in 2024, though at a more modest 0.4% reflecting the slow recovery in end-use markets. Output of agricultural chemicals is expected to rise 2.6% with gains in both fertilizers and crop protection chemicals. Production of consumer products which grew strongly last year will continue to expand at a slower 2.5% this year. In 2025, we expect both basic specialty chemical output to rise by 2.1%. Agricultural chemicals and consumer products will also continue to expand by 0.9% and 1.5% respectively.

The longer-term outlook for U.S. chemistry is positive with the natural gas liquids feedstock advantage continuing to favor U.S. production for the foreseeable future. Capacity expansions in customer industries motivated by recent legislation (e.g., IRA, IIJA, CHIPS) will create demand for U.S. chemistry. In addition, shortening of supply chains and the impact of Section 301 tariffs have motivated new investment in Mexico and the re-/near-shoring of manufacturing that will strengthen the North American manufacturing base. Because Mexico and Canada are the industry’s largest trading partners, expansion in Mexican manufacturing bodes well for U.S. chemical.

U.S. chemicals exports are projected to rise 3.1% this year (2024) following a decline over 2023. A stronger global economic environment and higher industrial activity will support our projections for steady, modest expansion in chemicals exports over the coming years. U.S. chemical imports will also rise this year, growing by 7.1%. Chemical imports growth is expected to cool to a solid 4-5% annual pace of growth over our forecast period. The U.S. continues to maintain a trade surplus in chemicals throughout the forecast horizon. Trade expansion is vulnerable to policy risks.

Growth in capital spending is expected to slow to 2.3% as higher borrowing costs dampen investment. Between 2025 and 2028, capex is expected to grow on average by 3.5% per year. While investment continues in shale-advantaged projects, a larger share of capex budgets are dedicated to clean energy and circular economy investments.

Following strong gains in 2022, chemical industry employment eased in 2023 and is expected to continue to drift lower in 2024 (by 1,800) before stabilizing in 2025 at around 553,000.

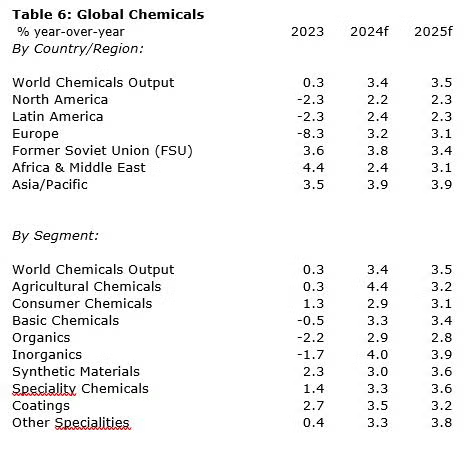

Globally, chemical production is expected to expand by 3.4% in 2024 with gains across all major regions. The largest gains will be in Asia/Pacific, former Soviet Union economies and Europe. Growth continues into 2025 with global volumes up by 3.5%.

Longer-Term Outlook & Risks

Prospects for U.S. chemistry remain positive with competitive energy fundamentals and the resurgence in U.S. manufacturing from once-in-a-generation legislative initiatives to promote clean energy, infrastructure, and a strong domestic manufacturing base.

One of the largest risks to this outlook, however, is the rising regulatory impact on the chemical industry in the U.S. that could undermine competitive advantages in energy and opportunities provided by the manufacturing expansion. If left unchecked, the dramatic rise in regulations focused on the chemical sector could incentivize companies and production to move offshore, potentially to parts of the world where chemical production is more carbon intensive.

In addition, policy missteps by the Fed (i.e., keeping rates higher for longer) new or escalating geopolitical conflicts, unexpected financial volatility, external shocks (i.e., weather, cyberattack, etc.) could also disrupt the outlook.

The full data set with historic trends and forecasts through 2027 is available to ACC members on ACCexchange and to others on the ACC Store.

Reasonable effort has been made in the preparation of this publication to provide the best available information. However, neither the American Chemistry Council, nor any of its employees, agents or other assigns makes any warranty, expressed or implied, or assumes any liability or responsibility for any use, or the results of such use, of any information or data disclosed in this material.