Running tab of macro indicators: 9 out of 20

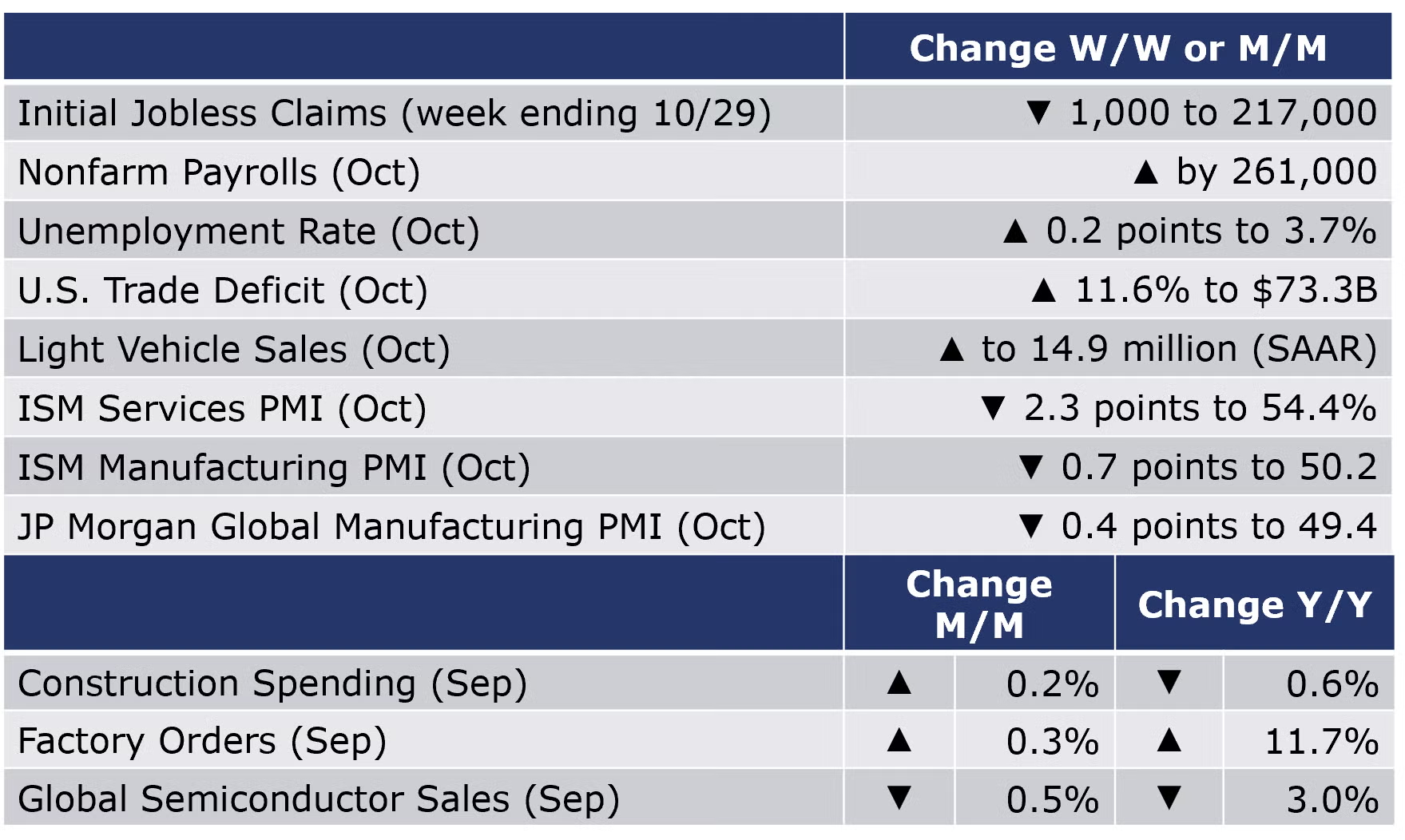

Once again, job growth surprised to the upside with nonfarm payrolls expanding by 261,000 in October, but there were some small signs of cooling. The pace of growth has slowed compared to the first half of the year and October’s gain was the lowest monthly increase since December 2020. Despite the slower pace of job growth, the increase was broad based with gains across nearly all major segments of the economy. Manufacturing added 32,000 jobs, the 18th consecutive gain. Average hourly wages grew by 4.7% Y/Y, the slowest pace since the end of last year. Separately, the unemployment rate rose by 0.2 percentage points off of its 50-year low to 3.7%. The decline reflects an increase in the number of unemployed people, as the size of the labor force edged slightly lower. The labor force participation rate continued to tick down to 62.2%, well below its pre-pandemic level.

The number of new jobless claims was down by 1,000 to 217,000 during the week ending 29 October. Continued claims were up 47,000 to 1.49 million for the week of October 22nd and the insured unemployment rate was 1.0%, unchanged from the previous week's rate.

Following a decline in August, the number of job openings rose to 10.7 million in September. Comparing the number of workers available in the economy (the civilian labor force) to the number of jobs (the number of employed people + the number of job openings), the economy continues to have a deficit of nearly 5 million workers. Compared against the number of unemployed people, there were 1.9 job openings per unemployed person in September.

Light vehicle sales continued their upward momentum from a 13.6 million seasonally adjusted annual pace to 14.9 million in October. There were increases in sales of both cars and light trucks. Vehicle sales were 12% above year-ago levels.

The U.S. goods and services trade deficit rose 11.6% in September to $73.3 billion as exports fell 1.1% and imports rose 1.5%. The gain in exports of capital goods (notably telecoms equipment and semiconductors) was not enough to offset declines in other sectors. Exports of industrial supplies and materials (including crude oil) and foods, feeds and beverages (including soybeans) decreased in September. Imports of goods rose in September driven by capital goods (semiconductors, telecoms equipment, and civilian aircraft) and consumer goods (e.g. cellphones and other household goods) and pharmaceutical preparations. Imports of industrial supplies and materials (including fuel oil, crude oil and other petroleum products) were down.

Construction spending rose 0.2% in September from August’s revised figure. Residential construction spending remained unchanged. Spending on multi-family home construction rose 0.3%, which was offset by a 2.6% decline new single family home construction. Non-residential spending increased 0.5% in September; the largest increase was for manufacturing (7.6%). Public spending on construction fell 0.4%, but with many infrastructure projects awaiting start and many local and state governments well-funded, the sector should remain resilient going forward.

According to the Institute for Supply Management (ISM), the Services PMI® for October 2022 registered 54.4%, 2.3 percentage points lower than September. Most (16 out of 18) U.S. non-manufacturing industries reported growth, but softness in business activity and new orders resulted in slower growth despite improved employment and supplier deliveries. This is the lowest reading of the composite index in 29 months, when the COVID recession hit. Based on comments from Business Survey Committee respondents, there have been improvements regarding supply chain efficiency and labor availability; however, performance remains less than ideal.

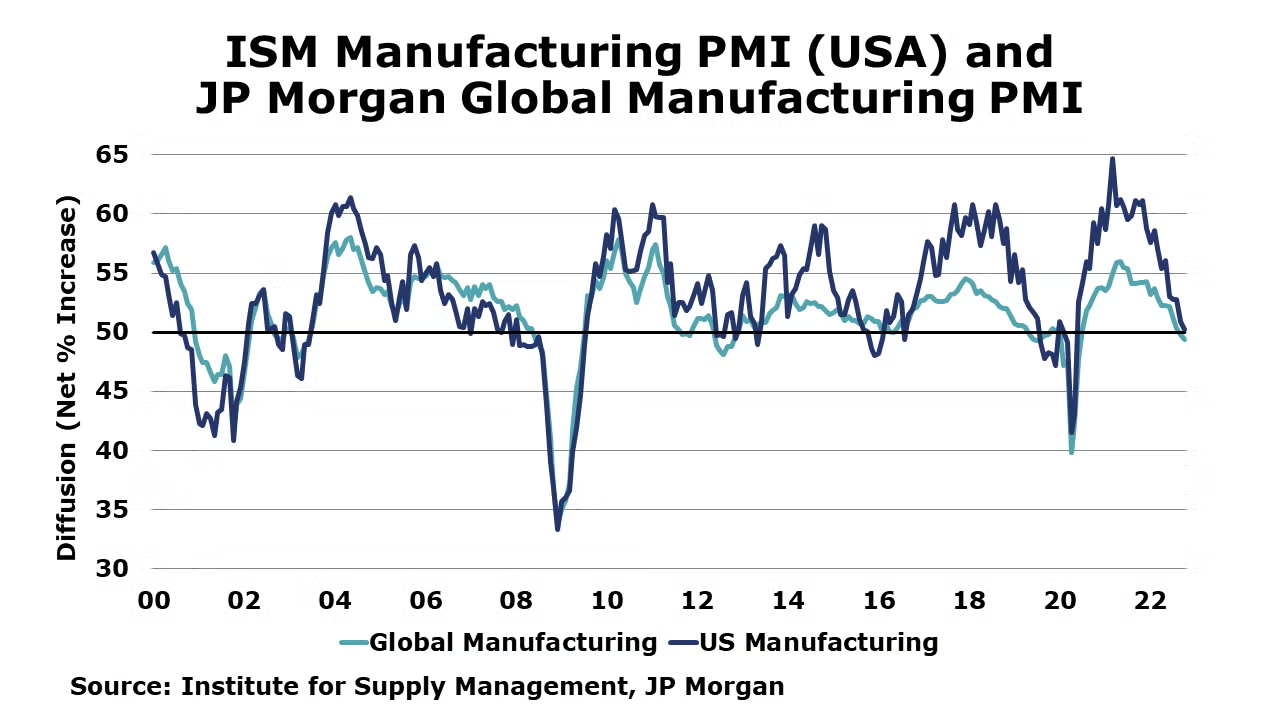

The ISM Manufacturing PMI fell 0.7 points to 50.2% in October, signaling the smallest rate of expansion in more than two years. A reading above 50 indicates that manufacturing expanded while a reading below 50 suggests that manufacturing activity contracted. New orders and new export orders continued to contract, and order backlogs contracted, suggesting a softening demand outlook. Production expanded at a faster pace in October, however. Manufacturers inventories expanded at a slower pace while customers’ inventories continue to be deemed “too low.” The prices index indicated decreasing prices for the first time since May 2020. Of the 18 industries covered, only eight reported growth in October.

The JP Morgan Global Manufacturing PMI indicated contraction in global manufacturing activity for the second month in a row as the index declined from 49.8 in September to 49.4 in October. The index has been on a general downward trend since about mid-2021 though it remained in growth territory (above the 50-mark) until recently. The downturn in centered in the intermediate goods stage while the PMIs for consumer and investment goods remain just above 50. Overall, global industrial production is contracting as new orders and new export orders weaken. Inflation on inputs and outputs is growing but at a slower rate. Businesses are less optimistic about the near term. The manufacturing PMI indicated growth in 12 of 32 countries tracked. Together, the signs from this release point to weakening demand and lower production.

Factory orders continued to expand in September, up by an expected 0.3%. As seen in last week’s durable orders report, much of the gain was centered in motor vehicles and civilian aircraft, however. Orders for consumer durables rose, but there were declines in new orders for construction supplies, IT equipment, and defense capital equipment. A proxy for business investment – new orders for capital equipment excluding aircraft – fell 0.4%, the first monthly decline since February. Manufacturing shipments continued to edge higher, up 0.2%, the same pace as inventories. Inventories of materials and supplies accounted for all of the gain offsetting a decline in work-in-progress inventories and continued flat growth in inventories of finished goods. The inventories-to-shipments ratio was unchanged at 1.46 compared to August, but up from 1.51 last September.

Global semiconductor sales fell 0.5% in September, with declines most notable in other Asia/Pacific (except Japan) (-2.9%), and China (-3.0%), offsetting gains in the Americas (4.8%), Japan (0.5%), and Europe (0.1%). Compared to a year ago, sales increased in Europe (12.4%), the Americas (11.5%), and Japan (5.6%), but decreased in the Asia Pacific/All Other (-7.7%) region and China (-14.4%).

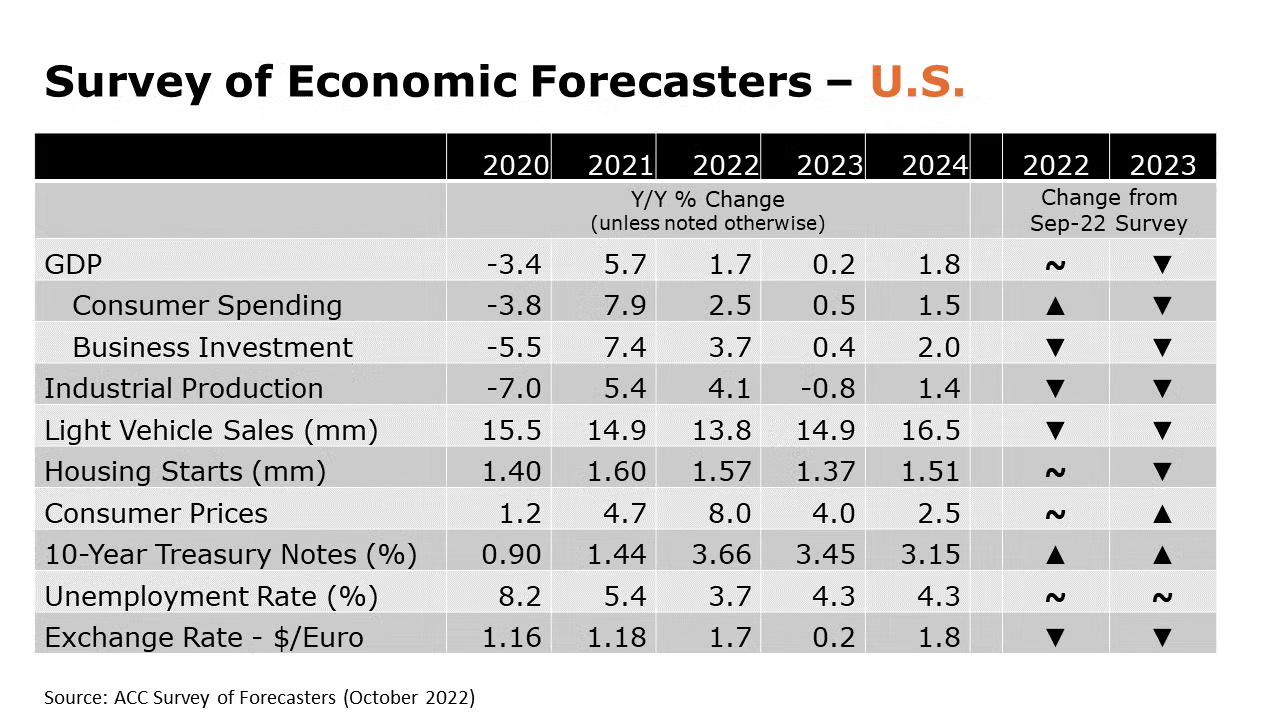

SURVEY OF ECONOMIC FORECASTERS

- The outlook for the rest of 2022 and 2023 continues to weaken as expectations rise for more aggressive interest rate hikes as the Fed seeks to get inflation under control. A recession seems likely to emerge in the first half of 2023.

- Expectations for U.S. GDP were steady with forecasters looking for a 1.7% gain in 2022. In 2023, forecasters are now expecting a 0.3% contraction in GDP as the U.S. economy slips into recession during the first part of the year.

- Consumer spending growth is expected to weaken to a 2.5% Y/Y pace in 2022 before falling by 0.2% in 2023.

- Business investment is expected to have grown by 3.7% in 2022. In 2023, growth in business investment slows further to a modest 0.4% gain, lower than last month’s forecast.

- With weaker growth in the second half of 2022, industrial production is expected to have risen 4.1% for the year as a whole and is expected to fall by 0.8% in 2023, a steeper decline than anticipated in last month’s survey.

- Higher borrowing costs and ongoing supply chain problems continue to constrain vehicle production and sales. As a result, expectations for light vehicle sales were lowered again to 13.7 million in 2022 (below 2020 when automakers were shut down for 2 months) and rising to only 14.9 million in 2023, well below trend.

- As mortgage rates have moved above 6%, expectations for interest rate-sensitive housing continue to show a lower level of homebuilding. Housing starts are expected to come in at 1.57 million in 2022 (same as last month’s survey), before slipping to 1.37 million in 2023.

- The unemployment rate is expected to average 3.7% in 2022 (unchanged from last month’s survey) and 4.3% in 2023, the same as in September’s survey.

- Expectations for gains in consumer prices remain at a four-decade high of 8.0% in 2022, before easing to an above-trend 4.0% pace in 2023, slightly higher than last month’s survey.

- Compared to last month, expectations for interest rates (10-year Treasury) rose as persistent inflation increases the likelihood of aggressive Fed tightening.

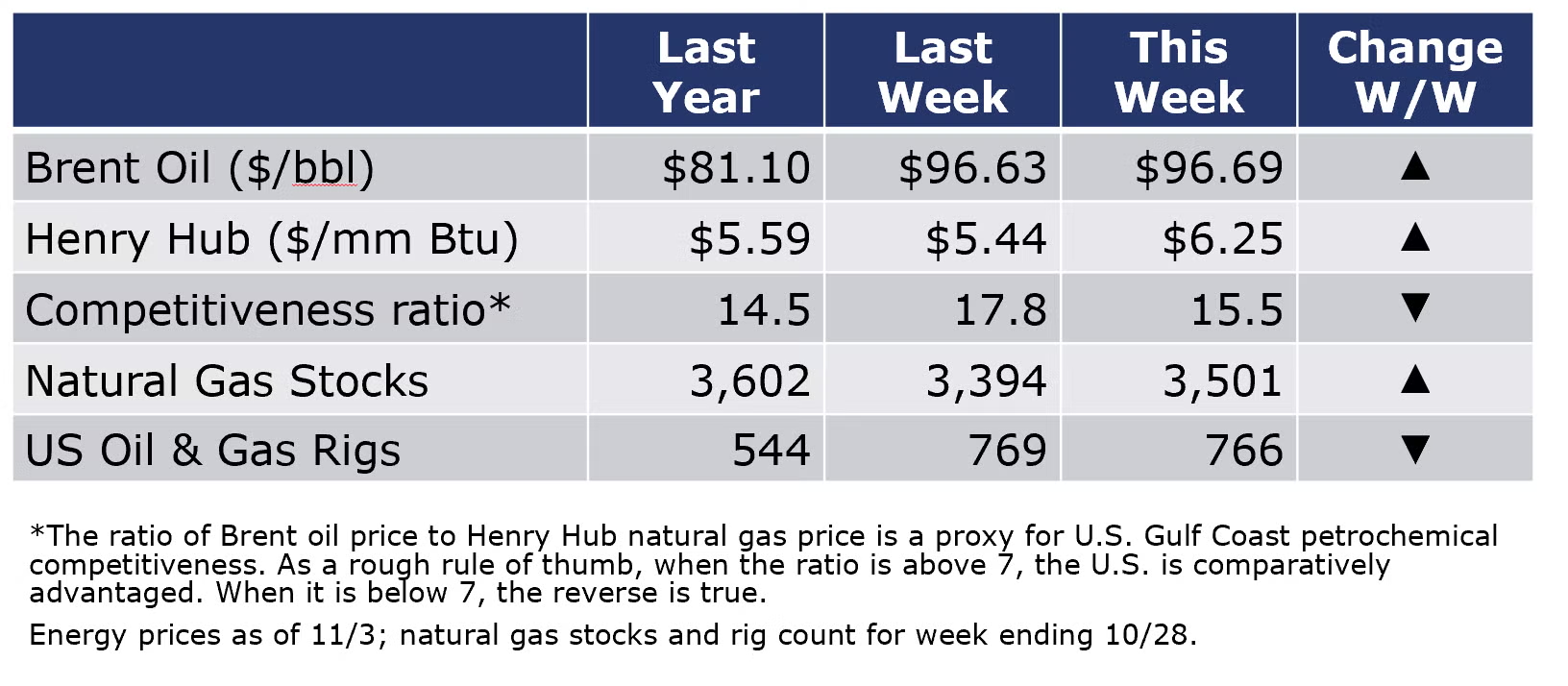

Oil prices were higher than a week ago as oil demand firmed. U.S. gas prices were stable, however.

For the business of chemistry, the indicators still bring to mind a yellow banner for basic and specialty chemicals.

Within the details of the ISM Manufacturing PMI, the chemical industry contracted in October with declines in production, new orders, export orders, order backlogs, imports, and inventories. Employment, however, expanded. Supplier deliveries were reported to be faster for chemical manufacturers. Plastic & rubber products was one of only three industries that reported growth in new orders. One chemical industry respondent noted that “customers are canceling some orders. Inventories of finished goods increasing.”

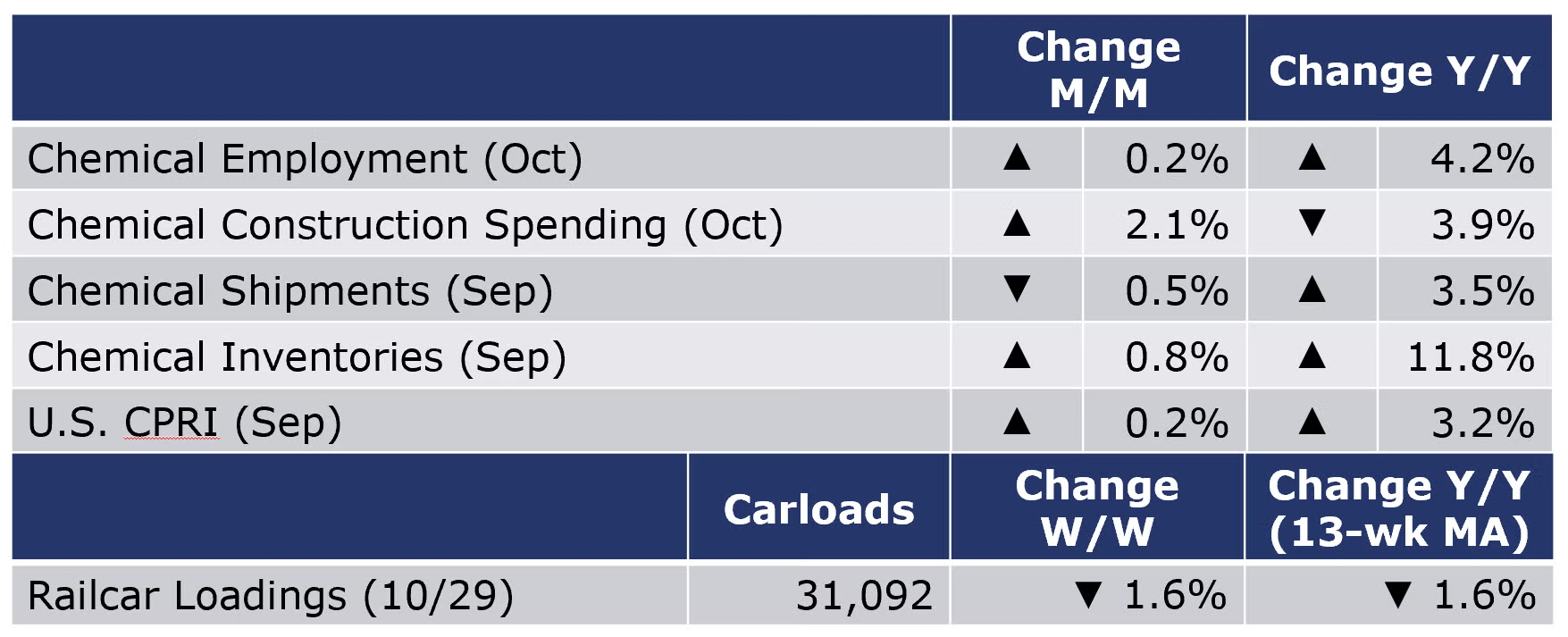

According to data released by the Association of American Railroads, chemical railcar loadings were down 1.6% to 31,092 during the week ending 29 October. Loadings were down 1.6% Y/Y (13-week MA), up 2.4% YTD/YTD and have been on the rise for 6 of the last 13 weeks.

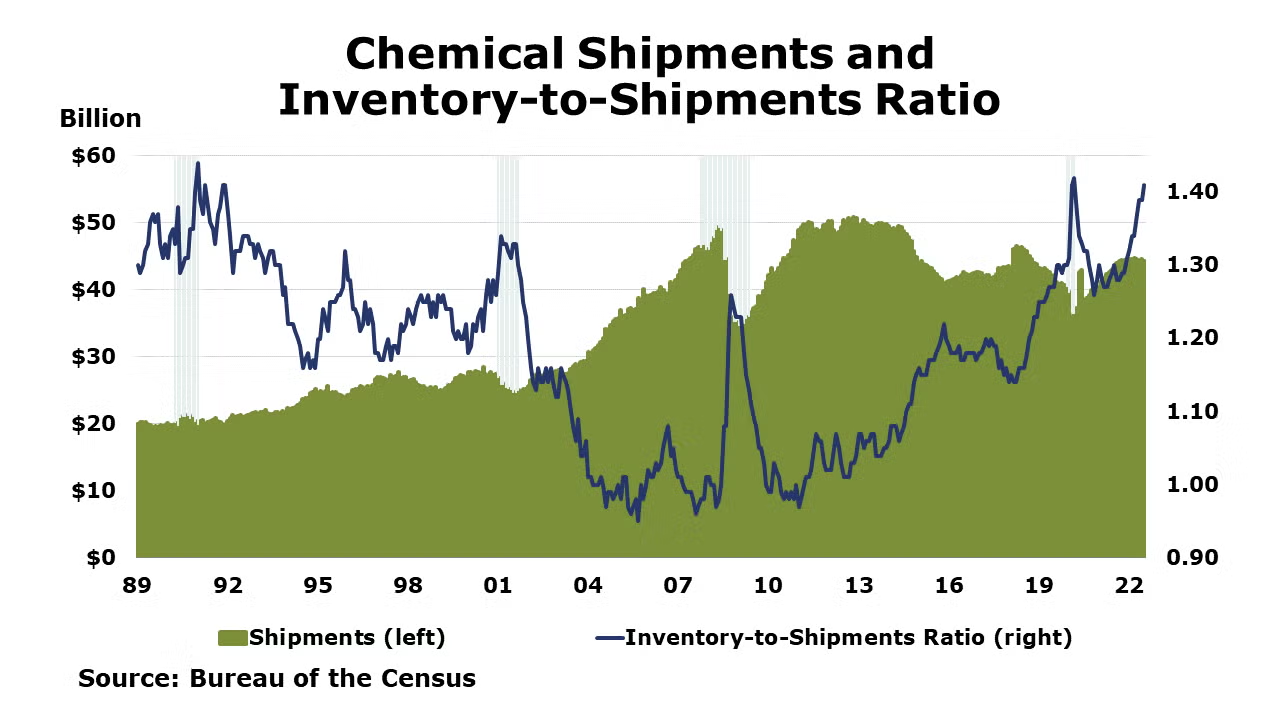

Following a 0.6% gain in August, chemical shipments fell 0.5% to $44.3 billion in September. Higher shipments of agricultural chemicals offset lower shipments of coatings, adhesives, and other chemical products. Chemical inventories continued to rise, however, up by 0.8% to $62.4 billion. Inventories rose across all major categories. It was the 22nd consecutive monthly gain in chemical inventories. The inventories-to-shipments ratio for chemicals rose from 1.39 in August to 1.41 in September, its highest level since May 2020. Shipments were up 3.5% Y/Y while inventories were up by 11.8% Y/Y, a sign of a growing imbalance.

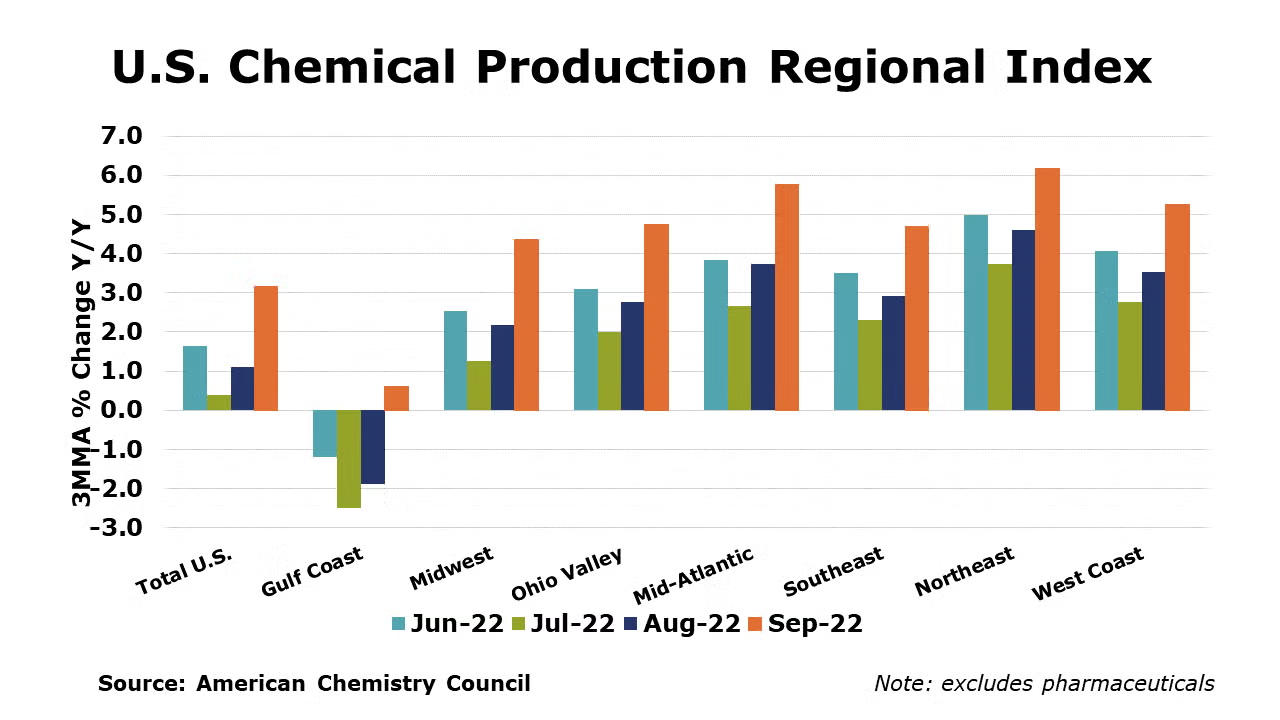

The U.S. Chemical Production Regional Index (U.S. CPRI) rose by 0.2% in September following 0.2% gains in July and August. Chemical output was mixed across regions with declines in the Gulf Coast region offset by higher production elsewhere in the country. The U.S. CPRI is measured as a three-month moving average (3MMA). Compared with September 2021, U.S. chemical production was ahead by 3.2% when chemical production was constrained due to Hurricane Ida. Chemical production was higher than a year ago in all regions.

On a 3MMA basis, chemical production within segments was mixed in September. There were gains in the production of coatings, adhesives, and other specialty chemicals; industrial gases; consumer products; synthetic dyes and pigments; and other inorganic chemicals. These gains were offset by lower production of plastic resins, organic chemicals, synthetic rubber, manufactured fibers, fertilizers and crop protection chemicals.

As nearly all manufactured goods are produced using chemistry in some form, manufacturing activity is an important indicator for chemical demand. Manufacturing output rose 0.5% in September (3MMA). The 3MMA trend in manufacturing production was mixed, with gains in the output of food & beverages, motor vehicles, aerospace, construction materials, fabricated metal products, machinery, computers & electronics, refining, foundries, oil & gas extraction, plastic products, rubber products, and apparel.

Chemical industry employment (including pharmaceuticals) grew by 1,600 (0.2%) in October with gains in both production workers and supervisory/non-production jobs. Compared to a year ago, chemical industry employment was higher by 36,400 (4.2%). Average hourly wages for production workers were off by 0.7% Y/Y, the first decline in nearly a year. The average workweek for chemical industry workers fell by 18 minutes in September to 41.0 hours and the total labor input into the chemical industry was 0.5% in October, consistent with the ISM report that suggested that the chemical industry output contracted.

The chemical industry construction spending edged up (2.1%) in September relative to August. On a year-to-year basis, spending is down 13.9%.

Note On the Color Codes

The banner colors represent observations about the current conditions in the overall economy and the business chemistry. For the overall economy we keep a running tab of 20 indicators. The banner color for the macroeconomic section is determined as follows:

Green – 13 or more positives

Yellow – between 8 and 12 positives

Red – 7 or fewer positives

For the chemical industry there are fewer indicators available. As a result we rely upon judgment whether production in the industry (defined as chemicals excluding pharmaceuticals) has increased or decreased three consecutive months.

For More Information

ACC members can access additional data, economic analyses, presentations, outlooks, and weekly economic updates through MemberExchange.

In addition to this weekly report, ACC offers numerous other economic data that cover worldwide production, trade, shipments, inventories, price indices, energy, employment, investment, R&D, EH&S, financial performance measures, macroeconomic data, plus much more. To order, visit http://store.americanchemistry.com/.

Every effort has been made in the preparation of this weekly report to provide the best available information and analysis. However, neither the American Chemistry Council, nor any of its employees, agents or other assigns makes any warranty, expressed or implied, or assumes any liability or responsibility for any use, or the results of such use, of any information or data disclosed in this material.

Contact us at ACC_EconomicsDepartment@americanchemistry.com